巴菲特2022股东信!十大重仓股曝光:苹果公司第一 比亚迪在列(全文)

独家抢先看

凤凰网财经讯 北京时间2月26日晚,“股神”巴菲特旗下投资公司伯克希尔·哈撒韦发布了一年一度的致股东信,财报显示,伯克希尔哈撒韦公布的去年四季度末前十大持仓分别为苹果(市值1611亿美元)、美国银行(市值459亿美元)、美国运通(市值248亿美元)、可口可乐(市236值亿美元)、穆迪公司(市值96亿美元)、威瑞森电信(市值82亿美元)、美国和众银行(市值80亿美元)、比亚迪(市值76亿美元)、雪佛龙(市值44亿美元)、纽约梅隆银行(市值38亿美元)。

伯克希尔哈撒韦第四季度净利润396.5亿美元 同比增10.6%

伯克希尔哈撒韦公司第四季度经营利润72.85亿美元,同比增45%,去年同期为50.21亿美元;第四季度的净利润396.5亿美元,同比增10.6%,上年同期为358.4亿美元;公司年地现金储备为1467.19亿美元。

巴菲特在致股东的信当中表示,伯克希尔将始终持有超过300亿美元的现金和等价物。巴菲特表示,伯克希尔在2021年增加其股票的内在价值方面取得了“合理的进展”;57年来,这一直是我的主要任务,并将继续如此。

2021年伯克希尔每股市值增幅为29.6% 跑赢标普500指数0.9个百分点

依照惯例,股东信开始还是伯克希尔的业绩与美股风向标标普500指数表现的对比,2021年伯克希尔每股市值的增幅是29.6%,标普500指数的增幅是28.7%,伯克希尔跑赢了0.9个百分点。

长期来看,1965-2021年,伯克希尔每股市值的复合年增长率为20.1%,明显超过标普500指数的10.5%,而1964-2021年伯克希尔的市值增长率是令人吃惊的3,641,613%,也就是36416倍多,而标普500指数为30209%,即超过302倍。

伯克希尔2022年已投入12亿美元回购股票

2022年以来,伯克希尔已投入12亿美元用于回购股票。2021年投入270亿美元用于回购股票。其中,2021年第四季度投入69亿美元回购股票。

标普500指数中表现最强的10家公司 有三家和巴菲特有关联

目前标普500指数中表现最强的10家公司,有三家和巴菲特有关联——首先就是伯克希尔公司,还有伯克希尔持股的美国银行和美国运通。

巴菲特:伯克希尔在2021年增加其股票的内在价值方面取得了“合理的进展”;57年来,这一直是我的主要任务,并将继续如此。

继续大手笔回购

在投资者较为关心的现金水平和回购计划方面,伯克希尔在四季度又回购了69亿美元的股票,使得去年全年整体回购金额达到270亿美元左右。作为参考,2020年伯克希尔刚创下全年247亿美元回购纪录。而2022年才过去近两个月,伯克希尔又投入12亿美元用于回购股票。

巴菲特解释称,目前公司内部业务的机会远超过并购,因此公司宁愿以回购的方式投资予自己公司。即便如此大手笔回购,伯克希尔的现金水平仍维持在1440亿美元的高位。其中1200亿美元投放在期限少于一年的美国国债。

年度股东大会日期确定

伯克希尔公司将于4月29日(周五)至5月1日(周日)在奥马哈举行年度股东大会。奥马哈急切地等待着你的到来,我也一样。

以下为全文:

Berkshire’s Performance vs. the S&P 500

伯克希尔哈撒韦业绩表现VS标准普尔500指数

Annual Percentage Change(年度百分比变化)

Year 年限 |

in Per-Share Market Value of Berkshire(伯克希尔每股市值) |

in S&P 500 with Dividends Included(包含股息的标准普尔 500 指数) |

1965 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

49.5 |

10.0 |

1966 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

(3.4) |

(11.7) |

1967 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

13.3 |

30.9 |

1968 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

77.8 |

11.0 |

1969 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

19.4 |

(8.4) |

1970 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

(4.6) |

3.9 |

1971 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

80.5 |

14.6 |

1972 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

8.1 |

18.9 |

1973 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

(2.5) |

(14.8) |

1974 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

(48.7) |

(26.4) |

1975 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

2.5 |

37.2 |

1976 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

129.3 |

23.6 |

1977 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

46.8 |

(7.4) |

1978 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

14.5 |

6.4 |

1979 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

102.5 |

18.2 |

1980 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

32.8 |

32.3 |

1981 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

31.8 |

(5.0) |

1982 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

38.4 |

21.4 |

1983 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

69.0 |

22.4 |

1984 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

(2.7) |

6.1 |

1985 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

93.7 |

31.6 |

1986 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

14.2 |

18.6 |

1987 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

4.6 |

5.1 |

1988 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

59.3 |

16.6 |

1989 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

84.6 |

31.7 |

1990 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

(23.1) |

(3.1) |

1991 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

35.6 |

30.5 |

1992 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

29.8 |

7.6 |

1993 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

38.9 |

10.1 |

1994 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

25.0 |

1.3 |

1995 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

57.4 |

37.6 |

1996 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

6.2 |

23.0 |

1997 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

34.9 |

33.4 |

1998 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

52.2 |

28.6 |

1999 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

(19.9) |

21.0 |

2000 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

26.6 |

(9.1) |

2001 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

6.5 |

(11.9) |

2002 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

(3.8) |

(22.1) |

2003 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

15.8 |

28.7 |

2004 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

4.3 |

10.9 |

2005 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

0.8 |

4.9 |

2006 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

24.1 |

15.8 |

2007 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

28.7 |

5.5 |

2008 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

(31.8) |

(37.0) |

2009 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

2.7 |

26.5 |

2010 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

21.4 |

15.1 |

2011 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

(4.7) |

2.1 |

2012 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

16.8 |

16.0 |

2013 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

32.7 |

32.4 |

2014 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

27.0 |

13.7 |

2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

(12.5) |

1.4 |

2016 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

23.4 |

12.0 |

2017 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

21.9 |

21.8 |

2018 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

2.8 |

(4.4) |

2019 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

11.0 |

31.5 |

2020 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

2.4 |

18.4 |

2021 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

29.6 |

28.7 |

Compounded Annual Gain – 1965-2021(1965年至2021年间复合年年度增长率) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

20.1% |

10.5% |

Overall Gain – 1964-2021(1964年至2021年间整总增长率) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

3,641,613% |

30,209% |

Note: Data are for calendar years with these exceptions: 1965 and 1966, year ended 9/30; 1967, 15 months ended 12/31.

BERKSHIRE HATHAWAY INC.

To the Shareholders of Berkshire Hathaway Inc.:

Charlie Munger, my long-time partner, and I have the job of managing a portion of your savings. We are honored by your trust.

Our position carries with it the responsibility to report to you what we would like to know if we were the absentee owner and you were the manager. We enjoy communicating directly with you through this annual letter, and through the annual meeting as well.

Our policy is to treat all shareholders equally. Therefore, we do not hold discussions with analysts nor large institutions. Whenever possible, also, we release important communications on Saturday mornings in order to maximize the time for shareholders and the media to absorb the news before markets open on Monday.

A wealth of Berkshire facts and figures are set forth in the annual 10-K that the company regularly files with the S.E.C. and that we reproduce on pages K-1 – K-119. Some shareholders will find this detail engrossing; others will simply prefer to learn what Charlie and I believe is new or interesting at Berkshire.

Alas, there was little action of that sort in 2021. We did, though, make reasonable progress in increasing the intrinsic value of your shares. That task has been my primary duty for 57 years. And it will continue to be.

伯克希尔·哈撒韦公司

致伯克希尔哈撒韦公司的股东:

查理·芒格(Charlie Munger),我一生的伙伴。我的工作是管理股东们的投资,我们很荣幸得到你们的信任。

如果我们是缺席本次股东大会的投资者而您是经理,我们有责任向你们通报我们想知道的内容。我们喜欢通过这封年度信函以及年度会议直接与你们交流。

我们的政策是平等对待所有股东。因此,我们不与分析师或大型机构进行讨论。此外,只要有可能我们还会在周六早上发布重要通讯,以最大限度地让股东和媒体在周一市场开盘前有时间吸收消化信息。

公司定期向美国证券交易委员会提交的年度10-K中列出了伯克希尔的大量事实和数据。并且我们在K-1到K-119页上进行了再现。一些股东会觉得这个细节很吸引人;其他人只会更喜欢学习查理和我认为在伯克希尔的新事物或有趣的事物。

2021 年几乎没有此类行动。不过,我们确实在提高股票的内在价值方面取得了合理进展。 过去57年来这项任务一直是我的首要职责,未来其还将继续如此。

What You Own

Berkshire owns a wide variety of businesses, some in their entirety, some only in part. The second group largely consists of marketable common stocks of major American companies. Additionally, we own a few non-U.S. equities and participate in several joint ventures or other collaborative activities.

Whatever our form of ownership, our goal is to have meaningful investments in businesses with both durable economic advantages and a first-class CEO. Please note particularly that we own stocks based upon our expectations about their long-term business performance and not because we view them as vehicles for timely market moves. That point is crucial: Charlie and I are not stock-pickers; we are business-pickers.

I make many mistakes. Consequently, our extensive collection of businesses includes some enterprises that have truly extraordinary economics, many others that enjoy good economic characteristics, and a few that are marginal. One advantage of our common-stock segment is that – on occasion – it becomes easy to buy pieces of wonderful businesses at wonderful prices. That shooting-fish-in-a-barrel experience is very rare in negotiated transactions and never occurs en masse. It is also far easier to exit from a mistake when it has been made in the marketable arena.

你们都拥有什么

伯克希尔拥有各种各样企业的所有权,有些是全部,有些只是部分。后者主要由美国主要公司的有价普通股组成。此外,我们拥有一些非美国股票,并参与了几家合资企业或其他合作活动。

无论我们采用何种所有权形式,我们的目标都是对具有持久经济优势和一流CEO的企业进行有意义的投资。请特别注意,我们持有股票是基于我们对其长期业务表现的预期,而不是因为我们将它们视为市场变动时候的应对工具。这一点很关键:查理和我不是选股者;我们是企业的甄选人。

我犯了很多错误。因此,我们广泛收集的业务对象包括一些具有真正非凡经济性的企业,许多其他具有良好经济特征的企业,以及少数处于边缘地位的企业。我们普通股部门的一个优势是——有时算是优势——很容易以优惠的价格购买优秀企业的股票。在谈判交易中,这种经历非常罕见,而且从未大量发生过。就算在市场上犯错,从错误中“撤退”也容易得多。

Surprise, Surprise

Here are a few items about your company that often surprise even seasoned investors:

• Many people perceive Berkshire as a large and somewhat strange collection of financial assets. In truth, Berkshire owns and operates more U.S.-based “infrastructure” assets – classified on our balance sheet as property, plant and equipment – than are owned and operated by any other American corporation. That supremacy has never been our goal. It has, however, become a fact.

At yearend, those domestic infrastructure assets were carried on Berkshire’s balance sheet at $158 billion. That number increased last year and will continue to increase. Berkshire always will be building.

• Every year, your company makes substantial federal income tax payments. In 2021, for example, we paid

$3.3 billion while the U.S. Treasury reported total corporate income-tax receipts of $402 billion. Additionally, Berkshire pays substantial state and foreign taxes. “I gave at the office” is an unassailable assertion when made by Berkshire shareholders.

Berkshire’s history vividly illustrates the invisible and often unrecognized financial partnership between government and American businesses. Our tale begins early in 1955, when Berkshire Fine Spinning and Hathaway Manufacturing agreed to merge their businesses. In their requests for shareholder approval, these venerable New England textile companies expressed high hopes for the combination.

The Hathaway solicitation, for example, assured its shareholders that “The combination of the resources and managements will result in one of the strongest and most efficient organizations in the textile industry.” That upbeat view was endorsed by the company’s advisor, Lehman Brothers (yes, that Lehman Brothers).

I’m sure it was a joyous day in both Fall River (Berkshire) and New Bedford (Hathaway) when the union was consummated. After the bands stopped playing and the bankers went home, however, the shareholders reaped a disaster.

In the nine years following the merger, Berkshire’s owners watched the company’s net worth crater from

$51.4 million to $22.1 million. In part, this decline was caused by stock repurchases, ill-advised dividends and plant shutdowns. But nine years of effort by many thousands of employees delivered an operating loss as well. Berkshire’s struggles were not unusual: The New England textile industry had silently entered an extended and non-reversible death march.

During the nine post-merger years, the U.S. Treasury suffered as well from Berkshire’s troubles. All told, the company paid the government only $337,359 in income tax during that period – a pathetic $100 per day.

Early in 1965, things changed. Berkshire installed new management that redeployed available cash and steered essentially all earnings into a variety of good businesses, most of which remained good through the years. Coupling reinvestment of earnings with the power of compounding worked its magic, and shareholders prospered.

Berkshire’s owners, it should be noted, were not the only beneficiary of that course correction. Their “silent partner,” the U.S. Treasury, proceeded to collect many tens of billions of dollars from the company in income tax payments. Remember the $100 daily? Now, Berkshire pays roughly $9 million daily to the Treasury.

惊喜,还是惊喜

以下是关于你们身为股东的企业的一些项目,即使是经验丰富的投资者也常常感到惊讶:

• 许多人认为伯克希尔是一个庞大且有些奇怪的金融资产集合。事实上,伯克希尔拥有和经营的美国“基础设施”资产——在我们的资产负债表上归类为财产、厂房和设备——比任何其他美国公司拥有和经营的都要多。这种霸权从来不是我们的目标,尽管这已经成为事实。

截至年底,这些国内基础设施资产以1580亿美元被计入伯克希尔的资产负债表。这个数字去年有所增加,并将继续增加。

• 每年,伯克希尔要缴纳大量联邦所得税。例如,在2021年我们支付了33亿美元,而美国财政部报告的企业所得税总收入不过为4020亿美元。此外,伯克希尔还缴纳大量州税和外国税。

伯克希尔哈撒韦的历史生动地说明了政府与美国企业之间无形且经常未被认可的金融伙伴关系。我们的故事始于1955年初,当时Berkshire Fine Spinning和Hathaway Manufacturing同意合并他们的业务。在请求股东批准的过程中,这些受人尊敬的新英格兰纺织公司对合并表示了很高的期望。

例如,Hathaway solicitation向其股东保证:“资源和管理的结合将导致纺织行业最强大、最高效的组织之一。”这种乐观的观点得到了公司顾问雷曼兄弟(是的,雷曼兄弟)的认可。

在合并后的九年里,伯克希尔的所有者目睹了公司的净资产从5140万美元降至2210万美元。这种下降的部分原因是股票回购、不明智的股息和工厂停工。但是,数千名员工九年的努力却造成了经营亏损。伯克希尔的挣扎并不罕见:新英格兰纺织业悄然进入了漫长且不可逆的死亡行军。

在伯克希尔和哈撒韦合并后的九年里,美国财政部也遭遇了伯克希尔的麻烦。总而言之,该公司在此期间仅向政府缴纳了337359美元的所得税——每天100美元,真是可怜。

时间到了1965年初,情况发生了变化。伯克希尔哈撒韦迎来了新的管理层,重新部署可用现金,并将基本上所有收益引导到各种良好的业务中,其中大部分业务多年来一直保持良好状态。将收益再投资与复利的力量结合起来,股东们获得了积极的回报。

应该指出的是,伯克希尔的所有者并不是该路线得以修正后的唯一受益者。他们的“沉默伙伴”美国财政部开始从该公司收取数百亿美元的所得税。还记得每天缴税100美元的时光吗?现在,伯克希尔每天向美国财政部支付大约900万美元税款。

In fairness to our governmental partner, our shareholders should acknowledge – indeed trumpet – the fact that Berkshire’s prosperity has been fostered mightily because the company has operated in America. Our country would have done splendidly in the years since 1965 without Berkshire. Absent our American home, however, Berkshire would never have come close to becoming what it is today. When you see the flag, say thanks.

• From an $8.6 million purchase of National Indemnity in 1967, Berkshire has become the world leader in insurance “float” – money we hold and can invest but that does not belong to us. Including a relatively small sum derived from life insurance, Berkshire’s total float has grown from $19 million when we entered the insurance business to $147 billion.

So far, this float has cost us less than nothing. Though we have experienced a number of years when insurance losses combined with operating expenses exceeded premiums, overall we have earned a modest 55-year profit from the underwriting activities that generated our float.

Of equal importance, float is very sticky. Funds attributable to our insurance operations come and go daily, but their aggregate total is immune from precipitous decline. When it comes to investing float, we can therefore think long-term.

If you are not already familiar with the concept of float, I refer you to a long explanation on page A-5. To my surprise, our float increased $9 billion last year, a buildup of value that is important to Berkshire owners though is not reflected in our GAAP (“generally-accepted accounting principles”) presentation of earnings and net worth.

为了公平对待我们的政府合作伙伴,我们的股东应该承认——实际上是大肆宣扬——伯克希尔的繁荣是因为公司在美国经营而得到了强有力的推动。自1965年以来,如果没有伯克希尔,我们的国家会做得非常出色。然而,如果没有我们的美国家园,伯克希尔永远不会接近今天的样子。当你看到国旗时,记得说声谢谢。

从1967年以860万美元购买National Indemnity开始,伯克希尔已成为保险“浮存金”领域的世界领先者——我们持有并可以投资但不属于我们的资金。包括来自人寿保险的相对较小的金额,伯克希尔的总流通量已从我们进入保险业务时的1900万美元增长到1470亿美元。

到目前为止,这类浮存金的成本比零还低。尽管我们经历过好几年保险亏损和运营费用超过保费的现象,但总体而言,我们从产生浮存金的承保活动中获得了55年的适度利润。

同样重要的是,浮存金非常具有粘性。保险业务的资金每天都在来来去去,但它们的总金额不会出现急剧下降。因此,在谈到投资的流动性时,我们可以从长远考虑。

如果您还不熟悉浮存金的概念,我建议您参阅第A-5页上的详细说明。令我惊讶的是,去年我们的流通股增加了90亿美元,尽管没有反映在我们的GAAP(“公认会计原则”)收益和净资产的表述中,但对伯克希尔所有者来说是很重要的价值积累。

Much of our huge value creation in insurance is attributable to Berkshire’s good luck in my 1986 hiring of Ajit Jain. We first met on a Saturday morning, and I quickly asked Ajit what his insurance experience had been. He replied, “None.”

I said, “Nobody’s perfect,” and hired him. That was my lucky day: Ajit actually was as perfect a choice as could have been made. Better yet, he continues to be – 35 years later.

One final thought about insurance: I believe that it is likely – but far from assured – that Berkshire’s float can be maintained without our incurring a long-term underwriting loss. I am certain, however, that there will be some years when we experience such losses, perhaps involving very large sums.

Berkshire is constructed to handle catastrophic events as no other insurer – and that priority will remain long after Charlie and I are gone.

Our Four Giants

Through Berkshire, our shareholders own many dozens of businesses. Some of these, in turn, have a collection of subsidiaries of their own. For example, Marmon has more than 100 individual business operations, ranging from the leasing of railroad cars to the manufacture of medical devices.

• Nevertheless, operations of our “Big Four” companies account for a very large chunk of Berkshire’s value. Leading this list is our cluster of insurers. Berkshire effectively owns 100% of this group, whose massive float value we earlier described. The invested assets of these insurers are further enlarged by the extraordinary amount of capital we invest to back up their promises.

我们在保险领域的巨大价值创造很大程度上归功于伯克希尔在我1986年聘用Ajit Jain时的好运气。我们第一次见面是在星期六早上,我很快就问Ajit他的保险行业从业经历是什么。他回答:“没有。”

我认为“没有人是完美的”并因此雇用了他。那是我幸运的一天:Ajit实际上是一个完美的选择。更好的是,35年后他仍然如此。

关于保险的最后一个想法:我相信伯克希尔的浮存金很可能——但远不能保证——可以在我们不招致长期承保损失的情况下维持。然而,我敢肯定某些年我们会经历这样的损失,可能涉及非常大的金额。

伯克希尔哈撒韦的设计宗旨是处理灾难性事件,这是其他保险公司所不具备的——而且在我和查理离开后很长一段时间内,这种优先级仍然存在。

我们的四大巨头

通过伯克希尔,我们的股东拥有数十家企业。其中一些又拥有自己的子公司。例如,Marmon拥有100多个独立的业务运营,从铁路车辆的租赁到医疗设备的制造。

• 尽管如此,我们“四大”公司的运营占伯克希尔价值的很大一部分。领先这个名单的是我们的保险公司集群。伯克希尔哈撒韦实际上拥有该集团100%的股份,我们之前描述过其巨大的浮动价值。

The insurance business is made to order for Berkshire. The product will never be obsolete, and sales volume will generally increase along with both economic growth and inflation. Also, integrity and capital will forever be important. Our company can and will behave well.

There are, of course, other insurers with excellent business models and prospects. Replication of Berkshire’s operation, however, would be almost impossible.

• Apple – our runner-up Giant as measured by its yearend market value – is a different sort of holding. Here, our ownership is a mere 5.55%, up from 5.39% a year earlier. That increase sounds like small potatoes. But consider that each 0.1% of Apple’s 2021 earnings amounted to $100 million. We spent no Berkshire funds to gain our accretion. Apple’s repurchases did the job.

It’s important to understand that only dividends from Apple are counted in the GAAP earnings Berkshire reports – and last year, Apple paid us $785 million of those. Yet our “share” of Apple’s earnings amounted to a staggering $5.6 billion. Much of what the company retained was used to repurchase Apple shares, an act we applaud. Tim Cook, Apple’s brilliant CEO, quite properly regards users of Apple products as his first love, but all of his other constituencies benefit from Tim’s managerial touch as well.

• BNSF, our third Giant, continues to be the number one artery of American commerce, which makes it an indispensable asset for America as well as for Berkshire. If the many essential products BNSF carries were instead hauled by truck, America’s carbon emissions would soar.

Your railroad had record earnings of $6 billion in 2021. Here, it should be noted, we are talking about the old-fashioned sort of earnings that we favor: a figure calculated after interest, taxes, depreciation, amortization and all forms of compensation. (Our definition suggests a warning: Deceptive “adjustments” to earnings – to use a polite description – have become both more frequent and more fanciful as stocks have risen. Speaking less politely, I would say that bull markets breed bloviated bull )

保险业务是为伯克希尔定制的。产品永远不会过时,销量一般会随着经济增长和通货膨胀而增加。此外,诚信和资本将永远重要。我们公司能够并且将会表现良好。

当然,还有其他具有出色商业模式和前景的保险公司。然而,复制伯克希尔的业务几乎是不可能的。

•苹果——我们以年终市值衡量的亚军巨人——是一种不同的持股方式。在这里,我们的所有权仅为5.55%,高于一年前的5.39%。但考虑一下,苹果2021年收入的每0.1%就达到1亿美元。我们没有花费伯克希尔的资金来获得我们的增长。苹果的回购起到了作用。

重要的是要了解,只有苹果公司的股息才计入伯克希尔的公认会计原则收益报告中——去年,苹果公司向我们支付7.85亿美元。然而,我们在苹果公司收益中的“份额”达到了惊人的56亿美元。公司保留的大部分资产用于回购苹果股票,我们对此表示赞赏。苹果杰出的CEO蒂姆·库克(Tim Cook)非常恰当地将苹果产品的用户视为他的初恋,但他的所有其他支持者也都受益于蒂姆的管理风格。

•BNSF,我们的第三个巨人,其仍然是美国业务的第一大动脉,这使它成为美国和伯克希尔不可缺少的资产。如果BNSF携带的许多基本产品改为用卡车运输,美国的碳排放量将会飙升。

你们投资的铁路在2021年的收入达到了创纪录的60亿美元。在这里,应该指出的是,我们谈论的是我们喜欢的老式收入:一个在利息、税收、折旧、摊销和所有形式的补偿之后计算得到的数字。

BNSF trains traveled 143 million miles last year and carried 535 million tons of cargo. Both accomplishments far exceed those of any other American carrier. You can be proud of your railroad.

• BHE, our final Giant, earned a record $4 billion in 2021. That’s up more than 30-fold from the $122 million earned in 2000, the year that Berkshire first purchased a BHE stake. Now, Berkshire owns 91.1% of the company.

BHE’s record of societal accomplishment is as remarkable as its financial performance. The company had no wind or solar generation in 2000. It was then regarded simply as a relatively new and minor participant in the huge electric utility industry. Subsequently, under David Sokol’s and Greg Abel’s leadership, BHE has become a utility powerhouse (no groaning, please) and a leading force in wind, solar and transmission throughout much of the United States.

Greg’s report on these accomplishments appears on pages A-3 and A-4. The profile you will find there is not in any way one of those currently-fashionable “green-washing” stories. BHE has been faithfully detailing its plans and performance in renewables and transmissions every year since 2007.

To further review this information, visit BHE’s website at brkenergy.com. There, you will see that the company has long been making climate-conscious moves that soak up all of its earnings. More opportunities lie ahead. BHE has the management, the experience, the capital and the appetite for the huge power projects that our country needs.

BNSF列车去年行驶了1.43亿英里,运送了5.35亿吨货物。这两项成就都远远超过任何其他美国铁路公司。你可以为你的铁路感到骄傲。

• BHE,我们的最后一个巨人,在2021年赚取了创纪录的40亿美元。与2000年(伯克希尔首次购买BHE股份的那一年)的1.22亿美元相比,增长了30多倍。现在,伯克希尔拥有该公司91.1%的股份。

BHE的社会成就记录与其财务业绩一样出色。该公司在2000年没有风能或太阳能发电。当时它被认为是庞大电力行业中一个相对较新和次要的参与者。随后,在David Sokol和Greg Abel的领导下,BHE已成为一个公用事业强国(请不要抱怨),并在美国大部分地区成为风能、太阳能和输电领域的主导力量。

Greg关于这些成就的报告出现在A-3和A-4页上。您将在那里找到的个人资料绝不是那些当前流行的“洗绿”故事之一。自2007年以来,BHE每年都忠实地详细说明其在可再生能源和输电方面的计划和表现。

要进一步查看此信息,请访问BHE的网站brkenergy.com。在那里,您会看到该公司长期以来一直在采取具有气候意识的举措,以实现其有收益。更多的机会将摆再面前, BHE对我国需要的大型电力项目拥有管理、经验、资金和投资意愿。

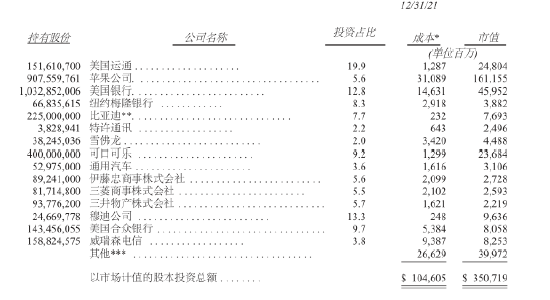

Investments

Now let’s talk about companies we don’t control, a list that again references Apple. Below we list our fifteen largest equity holdings, several of which are selections of Berkshire’s two long-time investment managers, Todd Combs and Ted Weschler. At yearend, this valued pair had total authority in respect to $34 billion of investments,

many of which do not meet the threshold value we use in the table. Also, a significant portion of the dollars that Todd and Ted manage are lodged in various pension plans of Berkshire-owned businesses, with the assets of these plans not included in this table.

12/31/21

投资

接下来让我们一起来讨论伯克希尔投资但并不拥有控股权的公司,在这里我们将再次提到苹果。以下是伯克希尔旗下前十五大持股投资,其中有几笔是伯克希尔的两位长期投资经理托德·康姆斯(Todd Combs)和泰德·韦斯切勒(Ted Weschler)的选择。截至2021年年底,这两位投资经理管理的总资产金额达到340亿美元,其中多项投资并未达到伯克希尔列表中使用的阈值。此外,托德和泰德管理的相当大一部分资金用于伯克希尔旗下企业的各种养老金计划,这部分资产并未包含在下表中。

2021年12月31日

股份 公司名称 公司持股比例 持股成本* 市值 (单位:百万)

151,610,700 美国运通公司 .................... 19.9 1,287 24,804

907,559,761 苹果. . . . . . . . . . . . . . . . . .5.6 31,089 161,155

1,032,852,006 美洲银行 ........................ 12.8 14,631 45,952

66,835,615 纽约银行梅隆公司. . . . . . . 8.3 2,918 3,882

225,000,000 比亚迪 **. . . . . . . . . . . . . . . .7.7 232 7,693

3,828,941 特许通讯. . . . . . . . . . . . . . 2.2 643 2,496

38,245,036 雪佛龙公司 . . . . . . . . . . . .2.0 3,420 4,488

400,000,000 可口可乐 . . . . . . . . . . . . . .9.2 1,299 23,684

52,975,000 通用汽车 . . . . . . . . . . . . . 3.6 1,616 3,106

89,241,000 伊藤忠商事株式会社. . . . . 5.6 2,099 2,728

81,714,800 三菱商事株式会社 . . . . . . 5.5 2,102 2,593

93,776,200 三井物产 . . . . . . . . . . . . . 5.7 1,621 2,219

24,669,778 穆迪公司.................. 13.3 248 9,636

143,456,055 美国合众银行. . . . . . . . . . 9.7 5,384 8,058

158,824,575 威瑞森通讯 . . . . . . . . . . . 3.8 9,387 8,253

其他*** .................................. 26,629 39,972

以市值计算的股本投资总额........ $ 104,605 $ 350,719

* This is our actual purchase price and also our tax basis.

** Held by BHE; consequently, Berkshire shareholders have only a 91.1% interest in this position.

*** Includes a $10 billion investment in Occidental Petroleum, consisting of preferred stock and warrants to buy common stock, a combination now being valued at $10.7 billion.

In addition to the footnoted Occidental holding and our various common-stock positions, Berkshire also owns a 26.6% interest in Kraft Heinz (accounted for on the “equity” method, not market value, and carried at $13.1 billion)

and 38.6% of Pilot Corp., a leader in travel centers that had revenues last year of $45 billion.

Since we purchased our Pilot stake in 2017, this holding has warranted “equity” accounting treatment. Early

in 2023, Berkshire will purchase an additional interest in Pilot that will raise our ownership to 80% and lead to our fully consolidating Pilot’s earnings, assets and liabilities in our financial statements.

* 实际持股成本,同时也是计税基础。

** 由 BHE 持有;因此,伯克希尔股东在该头寸中仅拥有 91.1% 的权益。

*** 包括对西方石油公司100亿美元的投资,具体包括优先股和购买普通股的认股权证,这一组合目前市值107亿美元。

除了注释中的西方石油和各种普通股的头寸,伯克希尔·哈撒韦公司还拥有卡夫亨氏26.6%的股权(按“股本”法计算,而非市值,账面价值为131亿美元)和Pilot公司38.6%的的股权。Pilot是一家旅行领域的领军企业,去年收入达到450亿美元。伯克希尔自2017年开始买入该公司股票,这部分投资在财务处理上已被计入“股权”项目。伯克希尔计划在2023年初将购买更多股份,将持股比例提升至80%,届时将在伯克希尔的财报中全面整合Pilot的收益、资产和负债。

U.S. Treasury Bills

Berkshire’s balance sheet includes $144 billion of cash and cash equivalents (excluding the holdings of

BNSF and BHE). Of this sum, $120 billion is held in U.S. Treasury bills, all maturing in less than a year. That stake leaves Berkshire financing about 1⁄2 of 1% of the publicly-held national debt.

Charlie and I have pledged that Berkshire (along with our subsidiaries other than BNSF and BHE) will always hold more than $30 billion of cash and equivalents. We want your company to be financially impregnable and never dependent on the kindness of strangers (or even that of friends). Both of us like to sleep soundly, and we want our creditors, insurance claimants and you to do so as well.

But $144 billion?

That imposing sum, I assure you, is not some deranged expression of patriotism. Nor have Charlie and I lost

our overwhelming preference for business ownership. Indeed, I first manifested my enthusiasm for that 80 years ago, on March 11, 1942, when I purchased three shares of Cities Services preferred stock. Their cost was $114.75 and required all of my savings. (The Dow Jones Industrial Average that day closed at 99, a fact that should scream to you: Never bet against America.)

After my initial plunge, I always kept at least 80% of my net worth in equities. My favored status throughout that period was 100% – and still is. Berkshire’s current 80%-or-so position in businesses is a consequence of my failure to find entire companies or small portions thereof (that is, marketable stocks) which meet our criteria for longterm holding.

Charlie and I have endured similar cash-heavy positions from time to time in the past. These periods are

never pleasant; they are also never permanent. And, fortunately, we have had a mildly attractive alternative during 2020 and 2021 for deploying capital. Read on.

美国国库券

伯克希尔的资产负债表包括1440亿美元的现金和现金等价物(不包括持有的BNSF和BHE),其中1200亿美元是美国短期国库券,到期时间不足一年。

在这里,我和查理承诺,伯克希尔(以及我们除BNSF和BHE以外的子公司)将始终持有超过300亿美元的现金和等价物。我们希望所有的投资人都能够在财务上坚不可摧,永远不要依赖其他人的仁慈。我们俩都喜欢高枕无忧,同时也希望我们的债权人、保险索赔人和投资人也同样如此。

至于1440亿美元,我在这里可以保证,这笔巨款绝不是爱国主义的疯狂表现,我和查理也没有失去对投资的热情。事实上,早在80年前的1942年3月11日,我第一次表现出自己对这一领域的热情。当时,我用自己所有的积蓄(114.75美元),购买了3股Cities Services的优先股。(道琼斯工业平均指数当天收于99点,这个事实应该会让人们大吃一惊:永远不要与美国打赌。)

在经历了最初的暴跌之后,我总是把至少80%的净资产投在股票上。在那段时间里,我最喜欢的状态是100%,到现在也依然如此。伯克希尔目前在股票方面的投资比例约为80%,这是因为我们还没有发现符合长期持有标准的目标。查理和我过去也曾出现过持有大量现金头寸的类似情况,处在这一期间并不愉快。幸运的是,在2020-2021期间,我们有了一个比较有吸引力的资金部署选择。

Share Repurchases

There are three ways that we can increase the value of your investment. The first is always front and center

in our minds: Increase the long-term earning power of Berkshire’s controlled businesses through internal growth or by making acquisitions. Today, internal opportunities deliver far better returns than acquisitions. The size of those opportunities, however, is small compared to Berkshire’s resources.

Our second choice is to buy non-controlling part-interests in the many good or great businesses that are

publicly traded. From time to time, such possibilities are both numerous and blatantly attractive. Today, though, we find little that excites us.

That’s largely because of a truism: Long-term interest rates that are low push the prices of all productive

investments upward, whether these are stocks, apartments, farms, oil wells, whatever. Other factors influence valuations as well, but interest rates will always be important.

Our final path to value creation is to repurchase Berkshire shares. Through that simple act, we increase your

share of the many controlled and non-controlled businesses Berkshire owns. When the price/value equation is right, this path is the easiest and most certain way for us to increase your wealth. (Alongside the accretion of value to continuing shareholders, a couple of other parties gain: Repurchases are modestly beneficial to the seller of the repurchased shares and to society as well.)

股票回购

我们可以通过三种方式增加投资人的投资价值,其中第一项一直是我们的首选,即:通过内部增长或并购增强伯克希尔控股业务的长期盈利能力。如今,内部机遇带来的回报远高于收购。然而,与伯克希尔的资源相比,这些机会的规模还不够大。

第二种方式是购买优秀上市公司的非控股权益。有时,这样的机会很多,但现在却很难找到让我们兴奋的企业。这在很大程度上是因为长期低利率会推高所有生产性投资的价格,无论这些投资是股票、公寓、农场还是油井等。其他因素也会影响估值,但利率始终很重要。

最后一种方式是回购股票。通过回购可以增加股东权益,在价值能够决定价格的情况下,这种方式是增加股东财富的不二选择。另外,股票回购不仅会增加长期股东的价值,还对出售股票的人以及社会都有一定的好处。

Periodically, as alternative paths become unattractive, repurchases make good sense for Berkshire’s owners.

During the past two years, we therefore repurchased 9% of the shares that were outstanding at yearend 2019 for a total cost of $51.7 billion. That expenditure left our continuing shareholders owning about 10% more of all Berkshire businesses, whether these are wholly-owned (such as BNSF and GEICO) or partly-owned (such as Coca-Cola and Moody’s).

I want to underscore that for Berkshire repurchases to make sense, our shares must offer appropriate value.

We don’t want to overpay for the shares of other companies, and it would be value-destroying if we were to overpay when we are buying Berkshire. As of February 23, 2022, since yearend we repurchased additional shares at a cost of $1.2 billion. Our appetite remains large but will always remain price-dependent.

It should be noted that Berkshire’s buyback opportunities are limited because of its high-class investor base.

If our shares were heavily held by short-term speculators, both price volatility and transaction volumes would materially increase. That kind of reshaping would offer us far greater opportunities for creating value by making repurchases. Nevertheless, Charlie and I far prefer the owners we have, even though their admirable buy-and-keep attitudes limit the extent to which long-term shareholders can profit from opportunistic repurchases.

Finally, one easily-overlooked value calculation specific to Berkshire: As we’ve discussed, insurance “float”

of the right sort is of great value to us. As it happens, repurchases automatically increase the amount of “float” per share. That figure has increased during the past two years by 25% – going from $79,387 per “A” share to $99,497, a meaningful gain that, as noted, owes some thanks to repurchases.

随着另外两种方式吸引力锐减,回购对伯克希尔的股东来说就显得尤为重要。因此,在过去两年中,我们总共回购了2019年底已发行股份的9%,价值517亿美元。本次回购让长期股东在伯克希尔全部业务中的权益增至10%以上,这些业务不仅包括伯克希尔旗下全资子公司,还包括可口可乐和穆迪等部分控股公司。

在这里我要强调,要使伯克希尔的回购有意义,回购价格必须细斟慢酌。如果在回购时定价过高,就会造成价值的损失。自去年底至2022年2月23日,伯克希尔回购的股票成本为12亿美元。我们还准备回购更多股票,但将始终取决于价格。

事实上,伯克希尔的回购机会并不多,因为我们拥有一流的投资者基础,然而在短期投机者大量持有的情况下,价格波动和交易量都会大幅增加,这种变动将为我们提供更多机会,通过回购来创造价值。不过,查理和我更喜欢我们现有的股东,即使他们在买入和持有方面的态度,限制了长期股东从回购中获利的程度。

最后,我还要再提一下伯克希尔特有的一个容易被忽视的价值计算,即:适当的保险“浮存金”对我们来说很有意义。回购会自动增加每股“浮存金”的金额,这一数字在过去两年中增长了25%,从A股每股79387美元增加到99497美元。如前所述,这在一定程度上归功于回购。

A Wonderful Man and a Wonderful Business

Last year, Paul Andrews died. Paul was the founder and CEO of TTI, a Fort Worth-based subsidiary of

Berkshire. Throughout his life – in both his business and his personal pursuits – Paul quietly displayed all the qualities that Charlie and I admire. His story should be told.

In 1971, Paul was working as a purchasing agent for General Dynamics when the roof fell in. After losing a

huge defense contract, the company fired thousands of employees, including Paul.

With his first child due soon, Paul decided to bet on himself, using $500 of his savings to found Tex-Tronics (later renamed TTI). The company set itself up to distribute small electronic components, and first-year sales totaled $112,000. Today, TTI markets more than one million different items with annual volume of $7.7 billion.

But back to 2006: Paul, at 63, then found himself happy with his family, his job, and his associates. But he

had one nagging worry, heightened because he had recently witnessed a friend’s early death and the disastrous results that followed for that man’s family and business. What, Paul asked himself in 2006, would happen to the many people depending on him if he should unexpectedly die?

For a year, Paul wrestled with his options. Sell to a competitor? From a strictly economic viewpoint, that

course made the most sense. After all, competitors could envision lucrative “synergies” – savings that would be achieved as the acquiror slashed duplicated functions at TTI.

But . . . Such a purchaser would most certainly also retain its CFO, its legal counsel, its HR unit. Their TTI

counterparts would therefore be sent packing. And ugh! If a new distribution center were to be needed, the acquirer’s home city would certainly be favored over Fort Worth.

一个了不起的男人和一项了不起的业务

去年,保罗·安德鲁斯(Paul Andrews)去世。保罗是伯克希尔沃斯堡子公司TTI的创始人兼首席执行官,为伯克希尔做出了卓越的贡献,我和查理都非常欣赏他。

1971 年,保罗在通用动力(General Dynamics)担任采购代理,该公司在失去一份重要的国防合同后,解雇了数千名员工,也包括保罗。就在此时,保罗的第一个孩子即将出生,他决定赌一把,用500美元积蓄创建了Tex-Tronics(后更名TTI)。Tex-Tronics成立之初的定位是销售小型电子元器件,第一年的销售额达到11.2万美元。如今,TTI的产品超过100万种,年销售额达77亿美元。

2006年,保罗在业务顺利发展之际却有一个挥之不去的担忧,尤其是在亲历一位朋友的早逝对其家庭和生意造成灾难性打击后,保罗的忧患意识进一步加强,并不断问自己,“如果意外身故,那些依赖自己的人将如何生存?”

一年来,保罗一直在寻找答案:卖给竞争对手?从严格的经济角度来看,这种选择最有意义。毕竟,竞争对手可以预见到利润丰厚的“协同效应”——当收购方削减TTI的重复职能部门时,可以实现这种节省。但是,这样的收购肯定还需要首席财务官、法律顾问和人力资源部门,而TTI的相关部门和人员将会被遣散。如果需要新部署,收购方所在城市肯定比沃斯堡更受青睐。

Whatever the financial benefits, Paul quickly concluded that selling to a competitor was not for him. He next considered seeking a financial buyer, a species once labeled – aptly so – a leveraged buyout firm. Paul knew, however, that such a purchaser would be focused on an “exit strategy.” And who could know what that would be? Brooding over it all, Paul found himself having no interest in handing his 35-year-old creation over to a reseller.

When Paul met me, he explained why he had eliminated these two alternatives as buyers. He then summed

up his dilemma by saying – in far more tactful phrasing than this – “After a year of pondering the alternatives, I want to sell to Berkshire because you are the only guy left.” So, I made an offer and Paul said “Yes.” One meeting; one lunch; one deal.

To say we both lived happily ever after is an understatement. When Berkshire purchased TTI, the company

employed 2,387. Now the number is 8,043. A large percentage of that growth took place in Fort Worth and environs.

Earnings have increased 673%.

Annually, I would call Paul and tell him his salary should be substantially increased. Annually, he would tell me, “We can talk about that next year, Warren; I’m too busy now.”

When Greg Abel and I attended Paul’s memorial service, we met children, grandchildren, long-time

associates (including TTI’s first employee) and John Roach, the former CEO of a Fort Worth company Berkshire had purchased in 2000. John had steered his friend Paul to Omaha, instinctively knowing we would be a match.

At the service, Greg and I heard about the multitudes of people and organizations that Paul had silently

supported. The breadth of his generosity was extraordinary – geared always to improving the lives of others,

particularly those in Fort Worth.

In all ways, Paul was a class act.

************

无论经济利益如何,保罗很快得出结论,出售给竞争对手不是自己的选择。接下来,保留考虑在金融业,也就是杠杆收购公司寻找买家。然而,保罗知道,这样的购买方将专注于“退出策略”。谁也不知道那会是什么?总而言之,保罗发现自己没有兴趣将35年的心血交给一家中间商。

在遇到我之后,保罗解释了自己为什么不考虑前两个选择,并表示在考虑了一年的其他方案后,想把公司卖给伯克希尔,因为我们是唯一的选择。在我提出一个条件后,我们达成了这笔交易。

当伯克希尔收购TTI时,该公司共有2387名员工,而如今这一数字已增长至8043,其中很大一部分增长发生在沃斯堡及其周边地区。与此同时,收益增长673%。

每年,我都会打电话给保罗,告诉他应该给他大幅加薪。而每一次,他都会告诉我,“我们可以明年再谈,沃伦。我现在太忙了。”

当格雷格·阿贝尔(Greg Abel)和我参加保罗的追悼会时,我们见到了他的家人和长期合作伙伴(包括TTI的第一位员工),以及约翰·罗奇(John Roach),他是伯克希尔在2000年收购的沃斯堡一家公司的前首席执行官。约翰把他的朋友保罗介绍给伯克希尔,本能地知道我们会成为伙伴。从各方面来说,保罗都是一个极为出色的人。

Good luck – occasionally extraordinary luck – has played its part at Berkshire. If Paul and I had not enjoyed

a mutual friend – John Roach – TTI would not have found its home with us. But that ample serving of luck was only the beginning. TTI was soon to lead Berkshire to its most important acquisition.

Every fall, Berkshire directors gather for a presentation by a few of our executives. We sometimes choose

the site based upon the location of a recent acquisition, by that means allowing directors to meet the new subsidiary’s CEO and learn more about the acquiree’s activities.

In the fall of 2009, we consequently selected Fort Worth so that we could visit TTI. At that time, BNSF,

which also had Fort Worth as its hometown, was the third-largest holding among our marketable equities. Despite that large stake, I had never visited the railroad’s headquarters.

Deb Bosanek, my assistant, scheduled our board’s opening dinner for October 22. Meanwhile, I arranged to

arrive earlier that day to meet with Matt Rose, CEO of BNSF, whose accomplishments I had long admired. When I made the date, I had no idea that our get-together would coincide with BNSF’s third-quarter earnings report, which was released late on the 22nd.

The market reacted badly to the railroad’s results. The Great Recession was in full force in the third quarter,

and BNSF’s earnings reflected that slump. The economic outlook was also bleak, and Wall Street wasn’t feeling friendly to railroads – or much else.

On the following day, I again got together with Matt and suggested that Berkshire would offer the railroad a

better long-term home than it could expect as a public company. I also told him the maximum price that Berkshire would pay.

Matt relayed the offer to his directors and advisors. Eleven busy days later, Berkshire and BNSF announced

a firm deal. And here I’ll venture a rare prediction: BNSF will be a key asset for Berkshire and our country a century from now.

The BNSF acquisition would never have happened if Paul Andrews hadn’t sized up Berkshire as the right

home for TTI.

这实在是一件很幸运的事情。如果保罗和我没有共同的朋友约翰·罗奇,TTI也不会成为伯克希尔的一员。但这份幸运仅仅是个开始,TTI很快将带领伯克希尔完成了最重要的收购。

每年秋天,伯克希尔的董事们都会聚集在一起,听取高层报告。我们有时会根据最近收购的公司的所在地来选择地点,这意味着董事将会与新子公司的CEO见面,并了解更多被收购方的活动。

2009年秋天,我们选择了沃斯堡,以便参观TTI。当时,同样位于沃思堡的BNSF是我们的第三大控股公司。尽管压下重注,但我却从来没有去过该公司的总部。我的助理黛布·博萨内克(Deb Bosanek)将董事会的开幕晚宴安排在10月22日。与此同时,我安排在当天早些时候与马特·罗斯(Matt Rose)会面,他是BNSF的首席执行官,我一直很赞赏他的成就。当我确定这个日期的时候,我并不知道我们的聚会将与BNSF第三季度收益报告发布时间撞期。股市对该公司的业绩反应强烈,大衰退在第三季度全面爆发,BNSF的收益反映了这种衰退。经济前景也很黯淡,华尔街对铁路或其他很多公司并不看好。

第二天,我与马特再次会面,并提出伯克希尔将为BNSF提供更好的选择,比它作为一家上市公司所能做出的期望还要好,我将伯克希尔的底价给了他。马特将这一提议转达给BNSF的董事和顾问。11天后,伯克希尔和BNSF宣布交易。在这里,我将冒险做出一个罕见的预测:从现在起,BNSF将成为伯克希尔·哈撒韦公司和美国一个世纪以来的一项关键资产。

如果保罗·安德鲁斯没有将伯克希尔视为TTI的最终归宿,BNSF的收购就永远不会发生。

Thanks

I taught my first investing class 70 years ago. Since then, I have enjoyed working almost every year with

students of all ages, finally “retiring” from that pursuit in 2018.

Along the way, my toughest audience was my grandson’s fifth-grade class. The 11-year-olds were squirming in their seats and giving me blank stares until I mentioned Coca-Cola and its famous secret formula. Instantly, every hand went up, and I learned that “secrets” are catnip to kids.

Teaching, like writing, has helped me develop and clarify my own thoughts. Charlie calls this phenomenon

the orangutan effect: If you sit down with an orangutan and carefully explain to it one of your cherished ideas, you may leave behind a puzzled primate, but will yourself exit thinking more clearly.

Talking to university students is far superior. I have urged that they seek employment in (1) the field and (2)

with the kind of people they would select, if they had no need for money. Economic realities, I acknowledge, may interfere with that kind of search. Even so, I urge the students never to give up the quest, for when they find that sort of job, they will no longer be “working.”

Charlie and I, ourselves, followed that liberating course after a few early stumbles. We both started as parttimers at my grandfather’s grocery store, Charlie in 1940 and I in 1942. We were each assigned boring tasks and paid little, definitely not what we had in mind. Charlie later took up law, and I tried selling securities. Job satisfaction continued to elude us.

感谢

70年前,我教了我的第一堂投资课。从那时起,我几乎每年都喜欢与各个年龄段的学生一起交流,最终在2018年“退休”。

一路上,我最难对付的听众是我上五年级的孙子的那个班级。 11岁的孩子们在座位上扭来扭去,茫然地看着我,直到我提到可口可乐及其著名的秘密配方。一瞬间,每个孩子都举起手来,让我明白了“秘密”对孩子们来说是一种诱惑。

教学,就像写作一样,能够帮助我开发并理清自己的思路。查理称这种现象为猩猩效应:如果你和一只猩猩坐下来,仔细地向它解释自己的想法,也许猩猩并不懂,但你自己的思路无疑会更加清晰。

与大学生交流要好得多。我告诉他们在这一领域找工作,并且如果不急需钱的话,应该做出怎样的选择。我承认,经济现实可能干扰这种选择。尽管如此,我还是希望学生们永远不要放弃探索,因为当他们找到那种工作的时候,他们将不仅仅是在“工作”。

查理和我在经历了一些早期的挫折后,走上了这条寻找自我的道路。我们都曾在我祖父的杂货店里做兼职,查理是1940年,我是1942年。我们每个人都被分配了无聊的工作,薪水也很少,那绝对不是我们想要的工作。后来,查理开始从事法律工作,而我则尝试着卖证券。可是,我们仍然不够满足。

Finally, at Berkshire, we found what we love to do. With very few exceptions, we have now “worked” for

many decades with people whom we like and trust. It’s a joy in life to join with managers such as Paul Andrews or the Berkshire families I told you about last year. In our home office, we employ decent and talented people – no jerks.

Turnover averages, perhaps, one person per year.

I would like, however, to emphasize a further item that turns our jobs into fun and satisfaction - - - - working for you. There is nothing more rewarding to Charlie and me than enjoying the trust of individual long-term shareholders who, for many decades, have joined us with the expectation that we would be a reliable custodian of their funds.

Obviously, we can’t select our owners, as we could do if our form of operation were a partnership. Anyone

can buy shares of Berkshire today with the intention of soon reselling them. For sure, we get a few of that type of shareholder, just as we get index funds that own huge amounts of Berkshire simply because they are required to do so.

最后,在伯克希尔,我们找到了自己喜欢做的事情。除了极少数例外情况,我们现在已经与我们喜欢和信任的人在一起“工作”了几十年。与保罗·安德鲁斯或者我去年提到的伯克希尔大家庭的经理人共事,是一种生活乐趣。在伯克希尔总部,我们拥有富有才华而正直的员工,平均每年的人事变动率大约为一个人。

然而,我想强调另一个让我们的工作变得有趣和满足的事情,那就是为大家工作。对查理和我来说,没有什么比获得个人长期股东的信任更有意义。几十年来,加入我们的股东期望我们将成为他们资金的可靠托管人。

显然,我们不能选择股东,如果我们的经营形式是合伙企业,还有这种可能。如今,所有人都可以购买伯克希尔的股票,并打算很快再出售这些股票。当然,我们会有一些这样的股东,就像我们会有指数基金持有大量伯克希尔股票,只是因为它们必须这样做。

To a truly unusual degree, however, Berkshire has as owners a very large corps of individuals and families

that have elected to join us with an intent approaching “til death do us part.” Often, they have trusted us with a large – some might say excessive – portion of their savings.

Berkshire, these shareholders would sometimes acknowledge, might be far from the best selection they could have made. But they would add that Berkshire would rank high among those with which they would be most comfortable. And people who are comfortable with their investments will, on average, achieve better results than those who are motivated by ever-changing headlines, chatter and promises.

Long-term individual owners are both the “partners” Charlie and I have always sought and the ones we

constantly have in mind as we make decisions at Berkshire. To them we say, “It feels good to ‘work’ for you, and you have our thanks for your trust.”

The Annual Meeting

Clear your calendar! Berkshire will have its annual gathering of capitalists in Omaha on Friday, April 29th

through Sunday, May 1st. The details regarding the weekend are laid out on pages A-1 and A-2. Omaha eagerly awaits you, as do I.

I will end this letter with a sales pitch. “Cousin” Jimmy Buffett has designed a pontoon “party” boat that is

now being manufactured by Forest River, a Berkshire subsidiary. The boat will be introduced on April 29 at our Berkshire Bazaar of Bargains. And, for two days only, shareholders will be able to purchase Jimmy’s masterpiece at a 10% discount. Your bargain-hunting chairman will be buying a boat for his family’s use. Join me.

February 26, 2022 Warren E. Buffett

Chairman of the Board

然而,伯克希尔拥有一个非常庞大的个人和家庭团队,他们选择加入我们,并“至死不渝”。他们常常把一大笔钱交给我们,也有一些人可能会表示这只是他们储蓄的一部分。

这些股东有时会承认,伯克希尔可能远不是他们本可以做出的最佳选择。但他们会补充说,在他们最满意的投资对象中,伯克希尔永远排在前列。总体而言,那些对自己的投资感到满意的人,将比那些被不断变化的头条新闻、闲聊和承诺所激励的人获得更好的结果。

个人长期股东既是查理和我一直寻求的“伙伴”,也是我们在伯克希尔做决策时一直考虑的“合伙人”。我们想说的是“为你们‘工作’感觉很好,感谢你们的信任。”

年度股东大会

伯克希尔将于将于4月29日(周五)至5月1日(周日)在奥马哈举行年度股东大会。年会细节在A-1和A-2页。奥马哈急切等待您的莅临,我也一样。

让我以这样一段话结束今天的致股东信——我的堂弟吉米·巴菲特(Jimmy Buffett)设计了一艘浮桥“派对”船,目前由伯克希尔的子公司Forest River负责打造。这艘船将于4月29日揭开神秘的面纱,在这两天时间内,股东可以以10%的折扣购买吉米的杰作。你们喜欢抄底的主席会买一艘供家人使用。来,加入我。

2022年2月26日

沃伦·巴菲特

董事会主席